Following the crisis in Ukraine, self-sanctions against Russian oil by oil traders concerned about payment bottlenecks along with Russian oil import sanctions by Western economies increased the price of Brent crude from US$90.81/barrel (b) on 17 February 2022 to US$129.8/b on 8 March 2022. Anticipating a prolonged crisis, most forecasters have revised their oil price expectations for 2022. Prior to the crisis in January 2022, the Energy Information Administration (EIA) forecasted that Brent crude prices would average about US$75/b in 2022 and US$68/b in 2023. Growth in oil supply that exceeded growth in demand and inventory increases were expected to exert downward pressure on oil prices.

Production of crude was expected to increase by 5.5 million barrels per day (mb/d) in 2022 with the USA, Russia, and the OPEC (Oil Producing and Exporting Countries) accounting for 84 percent (4.6 mb/d) of the increase. Oil consumption was expected to increase by 3.6 mb/d with the USA and China accounting for 39 percent of consumption growth. Oil inventories were projected to increase by 0.5 mb/d in 2022.

However, after the military intervention in Ukraine in March, the EIA revised its Brent crude price forecast for 2022 to US$101/b (by more than US$30/b) and US$85/b for 2023. This forecast was made prior to the import bans on the Russian crude by the USA and other European countries which leaves the possibility of another upward revision open. Goldman Sachs revised its Brent price expectation for 2022 to US$138/b from US$98/b with the possibility of 1.6 mb/d of the Russian crude removed from the market. JP Morgan revised expectations to a high of US$125/b for 2022.

Macroeconomic Impact

Oil prices impact the Indian economy through various channels. In the short term, high crude prices could increase inflation if the increase in crude prices is passed through to the retail consumers. At the extreme, an inflation estimate of 4.5% for 2022-23 by the RBI (Reserve Bank of India) could increase by about 1% if oil prices remain at about US$100/b. The impact could be lower if oil price pass-through is curtailed by reducing taxes on petrol and diesel, but this will translate into an increase in India’s fiscal deficit. It is estimated that an increase of the current excise of INR27.9/litre (l) on petrol and INR21.9/l on diesel is reduced by INR7/l, the government could lose revenue of close to INR1 trillion even if consumption of petrol and diesel increases by 8-10 percent in 2022-23. This is over 6 percent of the estimated fiscal deficit of over INR16 trillion for 2022-23.

Supply-driven oil shocks contribute more to the increase in current account imbalances than demand-driven shocks, and the impacts of supply-driven shocks are closely related to the degree of energy dependence.

India’s current account deficit (CAD) could increase significantly if oil prices remain high for a longer period. Oil is a critical input to the Indian economy and in the short term, demand is inelastic to price which means that when oil price increases, the oil import bill increases proportionally. In 2020-21, oil accounted for over 20 percent of India’s total import bill. Oil imports alone contributed about 56 percent of the total trade deficit of over US$102 billion. In 2020-21 the average price of crude (Indian basket) was US$44.82/b. The price of the Indian basket of crude in the past 11 months is over US$83/b (not including March 2022) and the oil import bill for March 2021-January 2022 is US$114.141 billion compared to US$82.684 billion in 2020-2021.

Analysis of the past oil price shocks suggest that the nature of the oil shock matters in understanding the effects of oil price shocks. Oil shocks can be aggregate demand-driven, oil-specific demand-driven, or supply-driven as in the current case. Supply-driven oil shocks contribute more to the increase in current account imbalances than demand-driven shocks, and the impacts of supply-driven shocks are closely related to the degree of energy dependence. In a demand-driven oil shock, the impact on current account imbalance is weak because an increase in oil price comes from an increase in global economic activity. The conclusion is that the trade channel (rather than the asset valuation or exchange rate channels) represents the main adjustment mechanism to oil shocks. Increasing exports under current circumstances of geopolitical turmoil, high commodity prices, and supply chain bottlenecks will be challenging for India. A higher growth rate of GDP (gross domestic product), even if achieved, will not necessarily cushion the adverse effect of high oil prices. It is estimated that even a 1 percent increase in GDP growth rates will not change the ratio of CAD to GDP significantly.

In the longer term, a sustained increase in oil prices could have an impact on economic activity and output. A decrease in the productivity of the economy because of an increase in the cost of production could also negatively impact wages, employment, and eventually the purchasing power of households. Analysis of the correlation between oil price shocks and macroeconomic outcomes show only a weak correlation between oil price shock and economic output for India compared to other large oil importers. The possible explanation is that India’s industrial output is more dependent on domestic coal, but this cannot lead to complacency. In most of the past supply-driven oil shocks, India’s economy has slumped along with the rest of the world.

Higher for Longer?

Two factors contributed to India’s 1991 balance of payments crisis. One was the crisis in the Middle East and the consequent increase in oil prices which battered the current account. The second was the economic slowdown in India’s trading partners which added to the current account crisis. In 1991, the value of petroleum imports increased by US$2 billion to US$5.7 billion as a result of an increase in oil prices combined with an increase in the volume of oil imports. In comparison, non-oil imports increased only by 5 percent in value terms and 1 percent in volume terms. The rise in oil imports led to a sharp deterioration of the trading account which was already under pressure on account of the fall of the erstwhile Soviet Union which was India’s important trading partner. The rest was history.

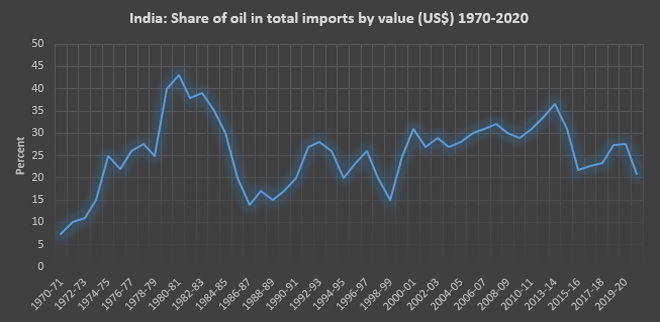

The share of crude in India’s total imports (in terms of value) has fluctuated in the last four decades reflecting changes in the global and domestic economy. In 1970, it was less than 10 percent but increased to more than 40 percent during the oil crises of the late 1970s. It has remained above 25 percent over the last two decades. Though this partly reflects an increase in consumption of oil, it also reflects higher oil prices (interrupted by the financial crisis in 2008 and the pandemic in 2019). In fact, during the pandemic, the narrative on oil prices centred around the theme “lower for longer”. In 2022, sanctions and uncertainty in the oil market appear to have changed the narrative to “higher for longer”. However, there is no certainty over this either.

By 17 March 2022, oil prices fell to about US$100/b from a high of over 130/b. This is attributed to a correction following speculative overshoot rather than a change in fundamentals. If oil prices remain higher for longer, it leads to demand destruction through an increase in efficiency of end-use and a shift to alternatives that brings prices down. But this takes time. The share of fossil fuels in the global primary energy basket fell from over 95 percent in 1965 to about 84 percent only in 2020. The share of oil in the global primary energy basket fell from over 41 percent to 34 percent in the same period but the geopolitics around oil appears to have held its ground. In 1956 the USA used its financial and military dominance to stop Anglo-French military action against the nationalisation of the Suez Canal by Egypt. Oil tankers were prevented from using the Suez Canal through which 1.2 million barrels of crude was carried each day. A major pipeline carrying half a million barrels of crude from Iraq through Syria was also sabotaged and exports of Middle Eastern oil to Britain and France were blocked. Surprised at their NATO (North Atlantic Treaty organisation) ally’s betrayal, several European countries turned to oil from the Soviet Union and in the 1970s gas from the Soviet Union. The irony to be noted by oil importers today is that more than 60 years later, oil’s strategic significance and oil importers’ (Europe’s) vulnerability has endured, though the roles of the perpetrator and saviour have reversed.

This article was first published on ORF.

Akhilesh Sati is the Program Manager for ORF Energy Initiative, Lydia Powell has been with the ORF Centre for Resources Management and Vinod Kumar has an MSc (Statistics) from Ramjas College, Delhi University. The views expressed in this article are those of the authors and do not represent the stand of this publication.

Read all the Latest Opinion News and Breaking News here

Comments

0 comment